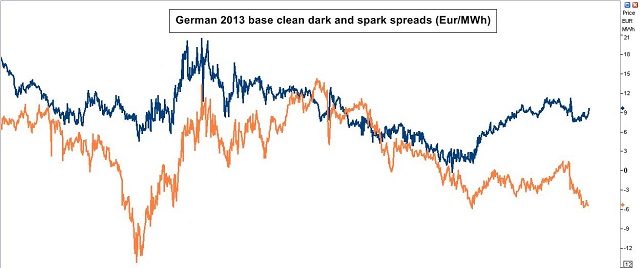

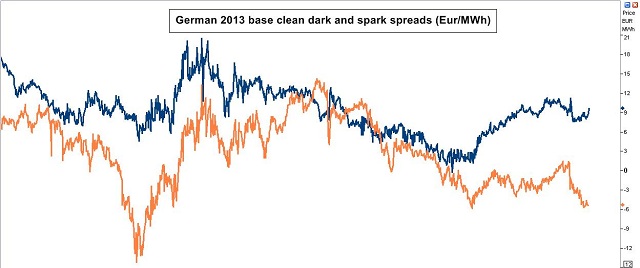

The pain being suffered by owners of European gas-fired power plant has escalated over the last 12 months. Weak power demand, subsidised renewable build and relatively high gas prices have conspired to crush gas fired generation margins, as shown in Diagram 1. It is difficult to imagine how market sentiment around gas-fired plant could get much worse.

About a year ago we questioned the prospect of a European gas plant bust in the form of plant mothballing, closures and the distressed sale of assets. There is clear evidence of a bust gathering steam in 2013, with a number of utilities pursuing exactly these actions.

The evidence

Recent announcements by European utilities indicate the pain that is being inflicted by weak gas plant generation margins. Importantly from a market overcapacity and asset value perspective, they also indicate significant action in response, in the form of mothballing, closures, strategic re-direction and in some cases asset sales. The following is a summary of utility announcements in Q1 2013:

- GDF Suez wrote down 2 billion euros worth of uneconomic gas plants in Europe. GDF recently took another 1.3 GW of capacity offline in addition to the 7.3 GW it has mothballed or closed since 2009. GDF’s CFO summarised the actions at an analyst conference last month, saying ‘It makes no sense to continue operating assets at a loss’.

- E.ON announced in January that is has scheduled 10GW of thermal assets to be decommissioned between 2012 and 2015, with E.ON’s CEO clear on his reasoning ‘We can’t just continue operating conventional plants in the hope something will change’.

- Vattenfall is engulfed in a domestic scandal after being forced to write down 17% of the value of its investment in Dutch utility Nuon. Vattenfall also stated its expectation that gas plant margins will not materially recover this decade.

- Centrica only broke even on its portfolio of UK gas-fired generation assets in 2012 and expects a £100m loss in 2013. In response it has announced the mothballing of Kings Lynn power station from April 2013 as it sees no improvement in spark spreads in the medium term. Centrica has re-configured the Peterborough, Brigg and Roosecote CCGTs to enable them to run in open-cycle mode.

- SSE has announced it will undertake extended maintenance at its 760MW Keadby and 688MW Medway plants in the UK, expecting them to be off line for at least a year.

- Barking Power is idling capacity at its 1 GW CCGT outside London on the expectation it will be unprofitable for the next couple of years.

- DONG announced a 27 percent writedown on its Severn CCGT in the UK as well as stating that it had only been able to operate its recently commissioned Dutch Enecogen CCGT plant and less than 10% load factor. DONG’s 2013 strategic statement also made it clear that it was pulling out of further investment in gas plant.

This is only a selection of recent announcements but the themes are consistent and clear.

The decision to hang on or walk away

The economics of an older gas plant is driven by the relationship between its market return and plant fixed costs, given capital costs have typically been paid down. Plant fixed costs can be thought of as the premium paid for ownership of a strip of sparkspread options. Gas plant owners are currently struggling to earn a plant return that covers this fixed cost premium, given the depressed level of market spreads and spread volatility.

In order not to mothball or close a plant in this environment, the owner needs to be able to convince themselves that the future value of plant flexibility outweighs its current inability to earn an adequate return. That decision is influenced by market sentiment which is currently very poor. There is also a game of ‘prisoners dilemma’ involved, in which plant owners who mothball and close capacity first, benefit other plant owners by reducing the capacity overhang in the market.

The painful part of the gas plant bust is underway as plants are closed and intrinsic value is either explicitly or implicitly written down to reflect a shift in market conditions. Weak sparkspreads may remain for a number of years, but this does not mean that older gas assets are worthless. The key to gas plant value is limiting fixed costs and maximising flexibility. This can be done using measures such as refining maintenance schedules, re-configuring the plant for open cycle operation and minimising gas connection costs. If technical or contractual constraints make this difficult then the best decision may be to close or mothball the asset.

But flexible gas plants can generate significant value from their ability to respond to changes in market prices (extrinsic value), even in a very weak spread environment. The challenge currently facing plant owners is how they can enhance, quantify and monetise that extrinsic value and whether it is high enough to justify keeping the plant open.