The Chinese have driven a hard bargain in closing a 38 bcma supply deal that is priced on a similar basis to Russia’s existing European supply contracts. But in return, Russia has secured a central role in supplying the Asian gas market over the next decade. Russia has also thrown down the gauntlet to LNG exporters courting China.

The Russia – China deal and the associated Power of Siberia pipeline should facilitate both:

- Future incremental sales of pipeline gas to China, both from Gazprom and potentially other Russian producers.

- The future export of Siberian gas from east coast Russian LNG terminals, on the doorstep of Asia’s largest buyers, Japan & Korea.

These factors present a substantial competitive threat to as-yet-uncontracted LNG producers in Australia, Canada and Africa, particularly given the higher combined production & shipping cost base of these exporters. The impact of the Russian deal in displacing Chinese LNG demand also increases the likelihood of the LNG oversupply scenario that we set out last month. As Russian gas starts to flow east later this decade, the Chinese border price could become an important benchmark in driving Asian gas pricing. China however may have other ideas.

Deal summary

Deal volume & infrastructure

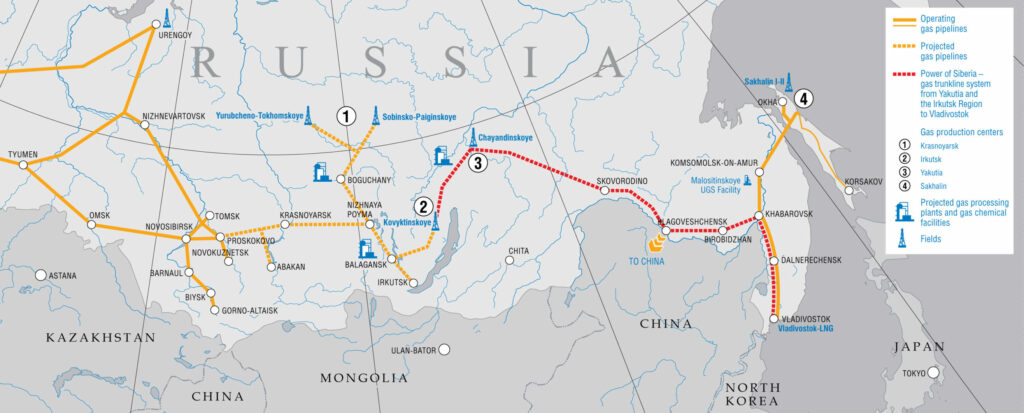

An initial agreement has been reached on 38bcma of gas, which will flow from Russia’s Eastern Siberian gas fields down a new ‘Power of Siberia’ pipeline into gas hungry North Eastern China. The pipeline within Russia is then planned to continue onto Vladivostok to support future Russian LNG exports. The route is shown in Chart 1 below:

The planned pipeline infrastructure may support up to 60 bcma over time. Wood Mackenzie estimates 125 bcma of gas demand in northern China by 2025, illustrating the growth potential through this and other pipelines.

The deal also opens up east coast Russian LNG exports. Volumes from the Kovyktinskoye and the Chayanda field could also supply gas to Gazprom’s proposed Vladivostok LNG project. And the pipeline also facilitates exports from other Russian producers.

But it is early days and there are large capex hurdles to be overcome before gas flow becomes a reality. The overall cost for the Kovyktinskoye and Chayandinskoye upstream development, Power of Siberia pipeline and processing costs could exceed $40 billion according to Woodmac.

Deal price

A range of analyst views on deal pricing have been circulating over the last two weeks. The headline reported deal price was somewhere between 350-380 $/tcm, equivalent to 9.5 to 10.4 $/MMBtu. But some analysts are estimating slightly higher contract prices by the time the gas flows in 2019 (up to around 11 $/MMBtu). The deal is oil-indexed and full pricing details have not been revealed, so all estimates are subject to uncertainty. There are also other factors in play that impact deal value e.g. the Russian vs Chinese share of pipe capex and upstream development costs.

But what is important is that the deal price, at somewhere around 10 $/MMBtu, is comparable to current German border prices for oil-indexed Russian contracts (after the various concessions granted to pricing formulae in recent years). This appears to be marginally cheaper than estimates of Turkmen gas at the Chinese border (11.00-11.50 $/MMBtu). And importantly, it is well south of recently signed Asian LNG contracts which are closer to 16 $/MMBTu at current oil prices.

The politics

Russia looks to have accepted price concessions to get the deal done at a time when Europe & the US are expressing concerns around security of supply from dependence on Russian energy exports. It is no coincidence that the deal has been struck in the midst of the political jousting around Ukrainian sovereignty.

But the Russians have exaggerated the level of competition for Russian gas. Gazprom CEO Alexei recently has stated that “Europe has lost the competition global for LNG, and in a single day it has just lost the competition for the world’s pipeline gas as well”. Talk like this makes impressive headlines back in Russia, but Russian exports are not a question of ‘either/or’ to Europe vs China. The gas for the Chinese deal is currently ‘stranded’ in east Siberia with no infrastructure linking it to the West Siberian producing province (which supplies Europe and which has some 100 bcma of excess production capacity). If there was really such a squeeze on Russian gas, China would not have been able to beat the deal price down to the extent that it has managed.

The deal is important to China but Russia is only one of a diversified mix of supply sources for the Chinese including:

- Domestic production – China has a substantial unconventional gas resources with the government targeting 80 bcma of shale gas production by 2020 (although realistically by 2020 production will likely fall well short of this).

- Turkmenistan, Uzbekistan & Kazakhstan pipeline gas – China is currently importing around 20 bcma a number that could triple by the start of next decade, and with potential to increase further if pipeline capacity can be expanded, given Turkmenistan’s massive reserves.

- LNG – China imported about 25 bcm in 2013 but is rapidly developing more regas capacity and is an investor in a number of upstream and liquefaction projects, both under construction and planned (e.g. in Australia, East Africa and Canada).

Nevertheless, it is reasonable to expect that the pricing of Russian pipeline gas may take on a very important role in influencing pricing in the evolving Asian gas market.

The importance of pricing

The new Russia-China deal at around 10 $/MMBtu (given current oil pricing) suggests Russia is at least initially willing to sell gas at the Chinese border at a similar price level to that of its European supply contracts. But the deal also facilitates development of Russian East coast LNG sales. For Russia this deal is a strategic enabler which allows them to:

- Increase future pipeline supply from East Siberian fields to China, at (what Russia hopes would be) higher price levels

- Export LNG to other Asian buyers via east coast terminals on ‘traditional’ oil indexed terms

- Potentially pave the way for the previously tabled Altai pipeline route to transport West Siberian gas into North West China – thus eventually monetising the 100 bcma or so of ‘surplus’ Russian production capacity

The recent Russia-China pipeline deal (which took 10 years to come to fruition) has clearly improved Russia’s current strategic positioning vis a vis the Asian market. However future developments in the wider supply arena and China’s future strategic positioning may frustrate some of Russia’s aims in this regard.

Firstly, the monetisation of 38 bcma of otherwise ‘stranded’ East Siberian gas represents a reduction in Asian LNG demand of 38 bcma of LNG (all other things being equal) and hence this volume will be available to challenge Russia’s pipeline gas market share in Europe.

Secondly, a mild European and Asian winter has seen European hub prices and Asian spot LNG fall sharply. And despite the outlook of a slow restart of Japanese nuclear plants, new supply is on the way with the PNG LNG project soon to start up and the first of many new Australian LNG projects coming onstream next year. As a result, sentiment is moving towards the ‘oversupply’ scenario that we set out in a recent article.

The Third factor is the degree of future success China has in creating supply options and competition, despite the likely continued rapid growth of its natural gas demand. In addition to further Russian pipeline supplies (from East and West Siberia) these include upside in Central Asian pipeline imports, shale gas development if successful, LNG projects with Chinese interests and future spot and contracted LNG supplies.

While Russia may be hoping that the pricing of volumes of Russian pipeline gas into China may become an important new Asian price benchmark, it is not clear that this suits China’s future requirements. China’s aims might be better served by maximising its own domestic production and creating competition between different pipeline gas supplies and LNG imports. It is quite possible that at some point in the next 5 to 10 years, China declares that all imports into the country be priced on a netback basis from its Shanghai hub, regardless of the aspirations of suppliers. Such a move is more likely to succeed in a well-supplied LNG market. The recent Russia – China 38 bcma pipeline deal ironically makes such an eventuality more achievable.

This week’s article included input from Howard Rogers, a Senior Advisor with Timera Energy and Director of Natural Gas Research at the Oxford Institute for Energy Studies.