The increasing level of gas hub indexation in European supply contracts has been a key factor behind the evolution of the gas market over the last 5 years. The momentum behind hub indexation has grown as North West European hub prices have consistently traded below oil-index contract levels since the financial crisis. This has acted to both develop hub liquidity and transparency as well as opening up a painful gap for suppliers between long term contract costs and short term retail contract pricing.

Whilst coming up with reliable assessments of the aggregate levels of gas indexation across European supply contracts is very difficult, there is undeniable evidence of an accelerating transition to hub indexation. But simple assessments of the levels of oil vs gas indexation overlook the dynamics that ensure that oil prices will be a key driver of hub price formation for many years to come.

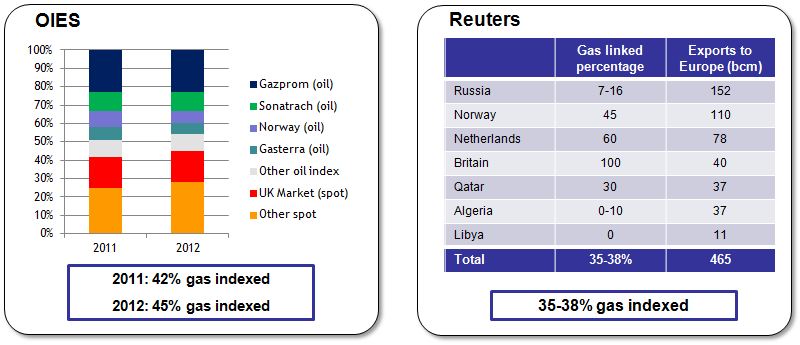

Current levels of gas indexation in Europe

The chart below shows recent OIES and Reuters assessments of the levels of gas indexation by European supply source.

Chart 1: Two views of aggregate European supply contract indexation

Source: Timera Energy based on data from Reuters and OIES (Oxford Energy Forum - August 2012)

As a third data point SocGen recently announced that they believe less than 50% of gas supplies will be linked to oil in 2013.

It is almost impossible to get an accurate assessment of gas indexation levels and growth. Most of the supply contracts are structural long term portfolio contracts with highly confidentially sensitive. Typically contract terms and conditions have evolved over time through the processes of renegotiation and price re-openers.

It also relatively easy to poke holes in the top down estimates above. For example, before the development of the NBP as a liquid hub, much of the gas coming into the UK from the North Sea was sold under long term contracts with strong components of oil indexation. While these contracts have mostly been de-dedicated from the field themselves and subject to many contract revisions over time, they still contain a large element of oil indexation. As a result it is optimistic to assume 100% of gas from the UKCS is gas linked. However, there is an undeniable trend of growth in gas indexation.

Gas vs oil indexation through the eyes of the re-opener

The gas vs oil debate has been in focus recently through the lens of re-opener negotiations and arbitrations. Here the key producers have taken opposite positions.

Statoil have been more willing to accept increased levels of indexation to NWE hubs and have stated that they expect the majority of their supplies in the future to be hub indexed. And they put their money where their mouth is last year by signing a 10 year 45 bcf supply deal with BASF primarily linked to the German hubs.

Gazprom and the North African producers have been more vociferous in their defence of oil indexation. Re-opener disputes have resulted in some concessions but these have been focused on temporary adjustments of absolute price levels. Gazprom have been very vocal in their public defense of oil indexation and have given only marginal concessions in terms of increased linkage to gas in reopener settlements with major NWE suppliers. However it is interesting to note that Gazprom, through its marketing and trading arm (Gazprom M&T), have signed a 3 year deal with Centrica to deliver 2.4 bcm gas to the UK entirely priced off the NBP.

If the Centrica deal is a sign of a strategic shift from Russia, then a more rapid transition to hub indexation is on the cards. But rather than this being an indication of a step change in position, it is more likely to be a result of Gazprom confronting the fact that, given the prevalence of gas indexation in UK wholesale and I&C contracts, it is almost impossible to find a buyer for an oil-indexed gas.

As the continental markets transition towards gas indexation as the standard for pricing sales to large end users, it becomes increasingly difficult for incumbent suppliers to bear misalignments between exposures in their supply contracts and retail portfolios. There has been a pronounced shift of large gas consumers on the continent following the long established UK precedent and requesting hub indexed gas as an alternative to standard fuel and gas oil formulas.

The influence of oil is here to stay

The original reasons for oil-indexation are mostly irrelevant to today’s European gas market. It is difficult to make a compelling commercial case for the retention of oil indexation as the predominant pricing influence. However, the influence of oil prices on European pricing dynamics will remain for many years.

Firstly, the legacy long term contracts (in some case 20+ years) that underpin most European pipeline imports are still predominantly oil-linked. The flexible volumes (typically above 85% take or pay) are a key source of marginal supply, allowing suppliers to manage overall portfolio balance. This means they will continue to have a disproportionate influence on hub pricing.

Secondly, much of the incremental supply will only flow into Europe against an oil linked threshold or opportunity cost alternative. In the coming years, un-contracted Russian production promises to be a key source of incremental supply which is likely to be strongly influenced by oil linked benchmarks. In addition, flexible LNG cargoes (divertible contract or spot purchases) will only flow into Europe if hub prices are higher than the best alternative on a netback basis. Asian LNG markets, which still have a strong linkage to crude, are likely to set that alternative for years to come.