Several structural trends are combining to change the way that LNG is being contracted. The traditional LNG contracting model was built on long term, destination specific, oil-indexed contracts between producers and suppliers. But a surplus of gas from the current supply glut is boosting the negotiation power of LNG buyers, who are seeking greater volume and pricing flexibility.

The LNG contracting market is maturing with a growing role of intermediary players and emerging market buyers. In parallel, there is a growing importance of hub market price signals as a benchmark from which to contract LNG. These trends point towards the evolution of a new contracting model to support the next wave of global LNG supply.

In this week’s article we look at 4 key trends that are driving an evolution of LNG contracting behaviour.

1. Reduction in average contract length

The financing of new LNG supply projects has traditionally been underpinned by long term, oil-indexed contracts (the most recent exampe of which is the Australian export contracts signed in the first half of this decade).

But this model is becoming increasingly challenging for LNG buyers who are confronted by a growing penetration of hub pricing. This is the same issue facing buyers of long term pipeline contracts. Mismatches between long term contract prices and hub prices are increasingly difficult to pass through to customers or to absorb into supplier portfolios.

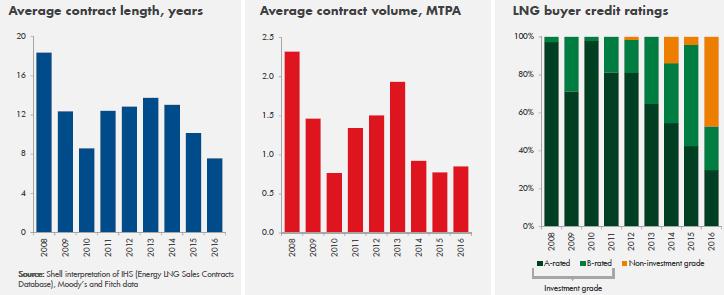

The supply glut has taken the pressure off LNG buyers to secure new supply via traditional long term contracts. Buyers in Asia, Europe and Latin America are instead pushing for shorter and more flexible gas linked contracts. This has driven a reduction in average contract length since the glut took hold in 2014. This can be seen in the left hand panel of Chart 1, taken from Shell’s 2017 LNG Outlook.

While the shift in contract negotiation power towards LNG buyers is an important factor behind reduced contract length, this trend is also supported by the other trends we set out below.

2. Growing importance of portfolio players

The role of LNG ‘intermediaries’ has grown rapidly over the last five years. These are primarily commodity trading companies (e.g. Vitol, Gunvor, Trafigura) who are focused on LNG midstream flexibility, with portfolios built around shorter term contract positions and access to shipping, regas and storage capacity. The growing role of these intermediaries is driving an important erosion of the direct contracting of LNG between producers and end suppliers.

Supply glut conditions are helping intermediaries gain traction in the LNG contracting market. Oversupply increases the availability of cargoes to trade, as well as strengthening the role of hub price signals against which portfolios can be managed. Access to flexibility is key to the business and contracting models of intermediary players. And that flexibility is being priced, hedged and optimised based on liquid hub price signals.

An example of the growing role of intermediaries was the large Egyptian tender in Nov 2016 (96 cargoes). The tender was dominated by intermediary players, with Glencore winning the largest volume, Trafigura also securing cargoes and Vitol and Gunvor providing competition.

3. Declining buyer credit quality

The right hand panel of Chart 1 shows a pronounced decline in the credit ratings of LNG buyers. This is a function of the evolving nature of LNG buyers. Traditional A-rated buyers (e.g. Japan, Korea) are currently relatively well contracted from long term deals signed pre-glut. In contrast, stronger demand growth from emerging buyers (e.g. India, Egypt, Pakistan) is acting to reduce credit quality.

Higher buyer credit risk is also a factor contributing to shorter contract lengths. Credit quality precludes a number of emerging buyers from contracting on a longer term basis. This has for example been an issue that has led Argentina to buy LNG via shorter term tenders.

Credit risk is further supporting the role of intermediaries in the LNG market. Commodity trading companies can often price & manage credit risk on a more competitive basis than producers, increasing their competitiveness in supplying LNG buyers. Some intermediaries also provide a ‘sleeving’ service for sale of individual cargoes, to insulate producers from the credit risk of emerging buyers.

4. Increasing penetration of hub prices

Hub prices drive pricing of end user gas sales in Europe and North America. As a result, there is a strong buyer preference for hub indexed LNG contracts.

So far there is an absence of liquid regional hubs as a reference in Asia and Latin America, although Singapore is making progress. But in a world of converged global gas prices, there is growing confidence in Atlantic basin spot price signals (NBP, TTF, Henry Hub) as a global benchmark for LNG contracting.

Even when LNG is contracted on an oil-indexed basis, the contract pricing terms are being set off liquid hub price benchmarks. Recent Middle Eastern tenders (e.g. Eygpt, Jordan) have been conducted on a Brent indexed basis, but with the level of oil-indexation effectively set off NBP & TTF spot price levels, given it is these hub prices driving the value of incremental LNG supply.

The importance of spot prices in the LNG market is penetrating much deeper than the exchange of contracts. Volumes of LNG cargoes transacted on a spot basis are still relatively low. But spot price signals are the key driver of LNG flow and optimisation decisions for large portfolio players, e.g. internal portfolio decisions such as cargo diversions and cargo swaps.

These portfolio optimisation activities impact a much larger volume of LNG than the external trading of cargoes. The importance of spot price signals is set to grow further as 89 bcma [65 mtpa] of highly flexible new US export supply is due online by 2021, most in 2018/19.

LNG buyers gaining influence over contract terms

In the tight post Fukushima LNG market, large buyers were pursuing individual strategies in competing to contract available incremental supply from producers in the US and Australia. But the supply glut has led to a more considered and collabrative approach.

Korean Kogas, Japanese JERA and China National Offshore Oil Corp (CNOOC) signed a memorandum of understanding this month to cooperate in the joint procurement of LNG. While this collaboration is no doubt aimed at sourcing lower priced LNG, Asian buyers are also pushing for greater flexibility in contract pricing and volume terms.

Market conditions favour the buyers. Our analysis shows the LNG market balance swinging relatively quickly from glut conditions to a tight market in the first half of next decade. This leaves producers in a challenging position, given 5 year lead times on new liquefaction projects.

The supply glut means that current market price signals are being driven by SRMC dynamics. So it is unlikely that LNG buyers will sign up to long term oil-indexed supply contracts at prices that support liquefaction project LRMC.

The negotiating power of LNG buyers will likely force greater market risk and contracting concessions onto producers (and the equity capital supporting new liquefaction projects). As the market tightens bargaining power will shift back towards producers. But by this stage, the traditional long term oil-indexed contracting model for new supply may be in terminal decline.

Article written by Olly Spinks & David Stokes