Last week we explored the impact of weaker Chinese LNG demand on European hub prices. We set out a scenario that illustrated the impact of European hubs having to absorb higher volumes of flexible LNG as the global balancing market.

This week we shift our focus to European gas demand. We aim to set out why European demand growth will be even more important than Asian LNG demand in driving the evolution of both European hub prices and spot LNG prices over the remainder of this decade.

European gas demand is a big deal

In the last 5 years gas demand across Europe has fallen by a staggering 19%. This equates to a 109 bcm reduction in annual demand from 585 bcm in 2010 to 476 bcm in 2014 (based on the IEA’s definition of Europe’s 32 gas consuming countries).

Putting this 5 year reduction in European demand in the context of the LNG market, 109 bcm represents more than 40% of total current annual Asian LNG demand. Approximately half of the fall in demand over the last 5 years occurred in 2014 alone (52 bcm), the result of exceptionally warm weather, e.g. Germany’s weather was the warmest in recorded history.

From these high level numbers, it is clear that the evolution of European gas demand over the remainder of this decade is a going to be a key driver of the global gas market balance. We will come back to look at the drivers of European gas demand in more detail in a separate article. But it is worth noting a few of the factors behind the decline:

- Fall in power sector gas demand as gas plant load factors have declined

- Relatively weak European economic growth

- Some structural reductions in demand e.g. energy efficiency improvements in residential gas demand (although these are small in size relative to the attention they have attracted)

Of these 3 factors, the power sector (1.) has been by far the largest contributor to the overall reduction in gas demand (once weather influences are accounted for). The fall in demand has been induced both by gas vs coal plant switching (given relatively weak coal prices) and by an increase in renewable output across Europe.

Looking forward, it is important to note the impact of extreme weather in 2014. Industry forecasters have been consistently overly optimistic in predicting a recovery in European gas demand. But it is reasonable to expect a significant demand recovery in 2015 regardless, given normalisation of the weather effects of 2014. This may also be supported by somewhat higher gas plant load factors as the result of weaker gas hub prices.

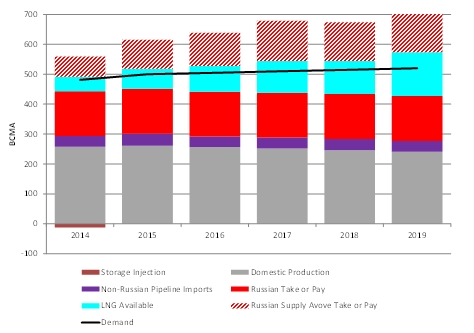

Demand growth and Europe’s ability to absorb LNG

In order to explore the impact of weaker European demand on hub prices, we use the same scenario framework we set out last week. We have defined what we see as a reasonable weaker gas demand growth scenario over the next 5 years as follows:

- European demand recovers by 27 bcm in 2015 as weather normalises, approximately half of the fall in demand from 2013 to 2014

- European demand then grows at an average of 0.75% from 2015-2020, primarily reflecting a recovery in power sector demand as the result of weaker gas hub prices

- That results in an annual demand of 522 bcma by 2020 (slightly less than the 2013 demand level) & can be contrasted with the more robust demand scenario we set out in April where demand recovered to 562 bcma by 2020

We combine this European demand scenario with an assumption that Asian LNG demand growth continues at a reasonably robust rate (18% CAGR), again as we assumed in the original LNG market scenario we set out in April.

The resulting impact on the European gas supply & demand balance is shown in Chart 1